BOOK KEEPING FORM 1

_1470040179220.png)

Subject Matter Of Book Keeping

Bookkeeping Form 1

Study Notes

Study Notes Discuss

Discuss Bookmarks

BookmarksThe Meaning of Book Keeping

Define book keeping

Book-keeping is an art of recording financial business transaction in a set of books in terms of money or money worth.

Bookkeeping involves the recording, storing and retrieving of financial transactions for a company, nonprofit organization and individuals.Prior to computers and software, the bookkeeping for small businesses usually began by writing entries into journals. Journals were defined as the books of original entry. In order to reduce the amount of writing in a general journal, special journals or day books were introduced. The special or specialized journals consisted of a sales journal, purchases journal, cash receipts journal, and cash payments journal.The image below shows purchase which was recorded in a day book. This was before the current development of communication technology.

Common financial transactions and tasks that are involved in bookkeeping include:

- Billing for goods sold or services provided to clients.

- Recording receipts from customers.

- Verifying and recording invoices from suppliers.

- Paying suppliers.

- Processing employees' pay and the related governmental reports.

- Monitoring individual accounts receivable.

- Recording depreciation and other adjusting entries.

- Providing financial reports.

Today bookkeeping is done with the use of computer software. For example, Quick-books (from Intuit) is a low-cost bookkeeping and accounting software package that is widely used by small businesses.

Bookkeeping requires knowledge of debits and credits and a basic understanding of financial accounting, which includes the balance sheet and income statement. In principle transactions have to be recorded daily into the books or the accounting system

For each transaction, there must be a document that describes the business transaction, in the terms of a simple sales invoice, sales receipt, a supplier invoice, a supplier payment, bank payments and journals.

Double-entry bookkeeping

The double entry system of bookkeeping is based upon the fact that every transaction has two parts and that this will therefore affect two ledger accounts.

Every transaction involves a debit entry in one account and a credit entry in another account. This serves as a kind of error-detection system: if, at any point, the sum of debits does not equal the corresponding sum of credits, then an error has occurred. Business transactions are events that have a monetary impact on the financial statements of an organization.

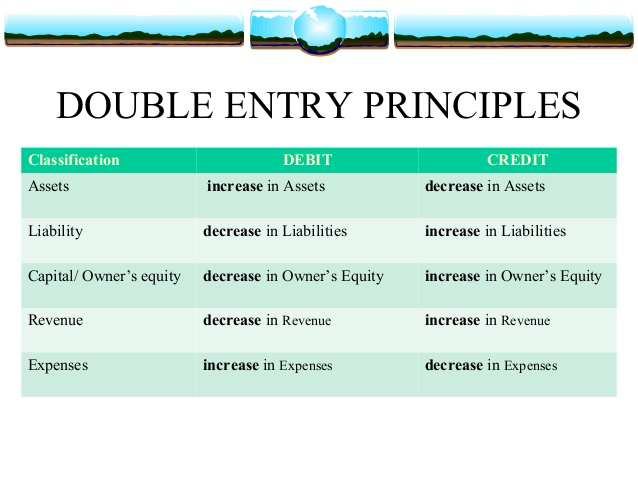

When accounting for these transactions, we record numbers in two accounts, where the debit column is on the left and the credit column is on the right. We always debit and credit financial transaction depending on what account your dealing with. For more information on double entry principle, see the table below.

- A debit is an accounting entry that either increases an asset or expense account, or decreases a liability or equity account. It is positioned to the left in an accounting entry.

- A credit is an accounting entry that either increases a liability or equity account, or decreases an asset or expense account. It is positioned to the right in an accounting entry.

The Role of Book Keeping

Explain the role of Book-keeping

View Teacher Notes

ASCERTAINMENT-To find out something(be sure/certain).

There are various objectives of bookkeeping and accounting to different parties i.e the owners, managers, creditors, government, customers etc. The common important objectives of book keeping are:

- Ascertainment of result of operation: Bookkeeping is intended to the ascertainment of the result of operation i.e the profit/loss of a firm or company by recoding all the revenue income and gains and expenses and losses of a certain period and by comparing them. It is ascertained by preparing the income statement or profit and loss account at the end of each fiscal year.

- Ascertainment of the financial position: It helps to ascertain the financial position of a firm or company by recording the appropriate values of different types of assets, specially in its net cost, and the capital and liabilities up to the date. It is found by preparing the balance sheet at the close of the fiscal year.

- Maintaining control over the assets and budget: Bookkeeping maintains control on the assets, income and expenses of all types by making their complete records. It helps one to see how efficiently the assets are utilized and the budget is disposed off. Thus, it establishes financial discipline by controlling frauds on budget and its expenditure.

- Prediction of the volume of cash for future: Bookkeeping helps the future forecast of cast by verifying the receipt and payments of an organization and the proposed expansion programmes. Specially, it is important to those whose financial system is based upon cash budget

Assessment of tax liabilities

Book keeping keeps the complete records of all business transactions and get them audited. Book keeping involves the income statement and balance sheet at the last of the fiscal year. It gives the details about the financial affairs of an organization, including the sales and net income on the basis of which tax liabilities i.e sales tax, income tax etc. can be easily assessed.

Importance and advantages of Bookkeeping

Book keeping is important to all, who are engaged in any sort of occupation and rather important to the organization for ascertaining the true state of the organization's affairs. The importance of book keeping may be studied with respect to different sectors.

- Important to the professionals and other individuals: Book keeping is important to the professionals like doctors, engineer, mechanics, lawyer, auditor etc. for recording their incomes and expenses and profits and losses etc. regularly and systematically for controlling expenses and gaining income. Similarly, it is important to the general people for making a proper balance of their income and expenses for their personal house hold affairs.

- Important to business organizations: Book keeping is essentially important to a business organization for keeping the complete records of the transactions. It is important, specially to determine the result of operation, financial position, controlling assets and other resources, establishing financial discipline, assessing tax liabilities etc.

- Important to the government: Book keeping is important to the government to evaluate the progress of the government projects, to collect necessary statements, data and information for the preparation of government budget, to control over the leakage, misuse and misappropriation of budget etc. of the government property and resources.

- Important to other parties: Book keeping is equally important to the financial analysts and other interested parties like investors, creditors, banks, customers etc. to study and analyze the different financial statements of a certain firm or company. It is also important to the job seekers for better opportunity for getting employment.

The Concept of Double Entry

Explain the concepts of business entity

View Teacher Notes

Transaction-Act of buying or selling something(exchange).

Every transaction has two effects. For example, if someone transacts a purchase of a drink from a local store, he pays cash to the shopkeeper and in return, he gets a bottle of drink. This simple transaction has two effects from the perspective of both, the buyer as well as the seller. The buyer's cash balance would decrease by the amount of the cost of purchase while on the other hand he will acquire a bottle of drink. Conversely, the seller will be one drink short though his cash balance would increase by the price of the drink.

Accounting attempts to record both effects of a transaction or event on the entity's financial statements. This is the application of double entry concept. Without applying double entry concept, accounting records would only reflect a partial view of the company's affairs. Imagine if an entity purchased a machine during a year, but the accounting records do not show whether the machine was purchased for cash or on credit. Perhaps the machine was bought in exchange of another machine. Such information can only be gained from accounting records if both effects of a transaction are accounted for.

Traditionally, the two effects of an accounting entry are known as Debit (Dr) and Credit (Cr). Accounting system is based on the principal that for every Debit entry, there will always be an equal Credit entry. This is known as the Duality Principal.

Debit entries are ones that account for the following effects:

- Increase in assets

- Increase in expense

- Decrease in liability

- Decrease in equity

- Decrease in income

Credit entries are ones that account for the following effects:

- Decrease in assets

- Decrease in expense

- Increase in liability

- Increase in equity

- Increase in income

Double Entry is recorded in a manner that the Accounting Equation is always in balance.

Assets - Liabilities = Capital

Any increase in expense (Dr) will be offset by a decrease in assets (Cr) or increase in liability or equity (Cr) and vice-versa. Hence, the accounting equation will still be in equilibrium.

LEDGER: Is a main book of account. Used to record all transaction in a systematic way or

A ledger is a complete record of financial transactions over the life of a company. The ledger holds account information that is needed to prepare financial statements, and includes accounts for assets, liabilities, owners' equity, revenues and expenses.

A general ledger is a complete record of financial transactions over the life of a company. The ledger holds account information that is needed to prepare financial statements, and includes accounts for assets, liabilities, owners' equity, revenues and expenses.

Posting is when the balances in sub ledgers and the general journal are shifted into the general ledger. Posting only transfers the total balance in a sub ledger into the general ledger, not the individual transactions in the sub ledger. An accounting manager may elect to engage in posting relatively infrequently, such as once a month, or perhaps as frequently as once a day

AN ACCOUNT: is a record in the general ledger that is used to collect and store debit and credit amounts. For example, a company will have a Cash account in which every transaction involving cash is recorded. If the company sells merchandise for cash, the Cash account will be debited and the Sales account will be credited.

Another definition of an account is a record of a customer relationship. For example, if a company sells merchandise to a customer on credit, the seller will have an account receivable and the purchaser will have an account payable.

The term on account means not for cash. For example, if a company purchases merchandise with the terms net 30 days, it means the company has 30 days in which to pay.

An account has two sides:

- DEBIT SIDE-is the left side of an account

- CREDIT SIDE-is the rightside of an account.

Exercise 1

Read carefully at the following sentences, decide whether it is true or false. Remember to refer to the notes

- Double entry involve two entries_______

- Debit side is on the right side of double entry account _____

- When using double account, you must always ignore the way banks treat their debit and credits _____.

- In double entry accounting, every transaction is recorded twice. _____.

- Example of payment into bank account is wages. _____

Principles Of Double Entry System

Bookkeeping Form 1

In these concept, you are going to explore more about business transactions. It is very important that, you understand about the basic principles of double entry system. Please watch the following video and remember to share your ideas on the discussion forum.

Please use a regular YouTube link.

Description of a Business Transaction

Describe what a business transaction is

Exercise 1

Do you know what steps to take when recording any business transaction? Here is the summarized accounting cycle

An accounting transaction is a business event having a monetary impact on the financial statements of a business. It is recorded in the accounting records of the business. Examples of accounting transactions are:

- Sale in cash to a customer, this is like when you go to shop and buy goods in exchange for money.

- Sale on credit to a customer. Credit sales are allowances of goods to customers in order to pay in advance.The name speaks for itself. It is goods given to a customer on credit, meaning that you sell the goods and collect cash at a later date per agreement with customer

- Receive cash in payment of an invoice owed by a customer. This is mostly used consultations nowadays. example, some one may be working to provide her skills on a project and she wrote an invoice to ask for payment after the end of the project. Import and exports use this kind of transaction too.

- Purchase fixed assets from a supplier

- Record the depreciation of a fixed asset over time

- Purchase consumable supplies from a supplier

- Investment in another business

- Investment in marketable securities

- Engaging in a hedge to mitigate the effects of an unfavorable price change

- Borrow funds from a lender

- Issue a dividend to investors

- Sale of assets to a third party

Analysis of a Business Transaction

Analyses a business transaction

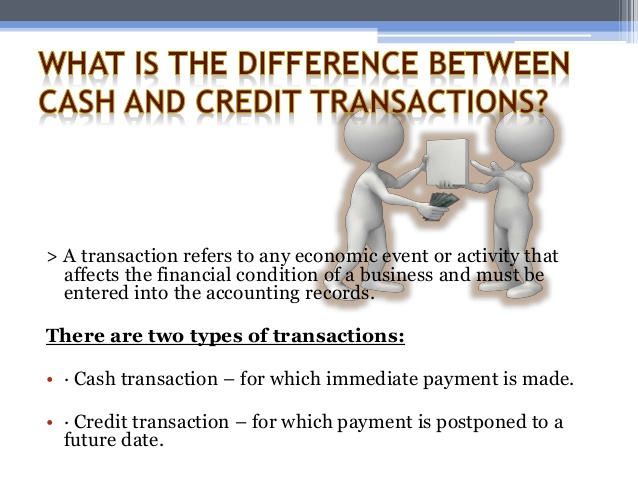

What’s the difference between a cash and credit transaction?The only difference between cash and credit transaction is the timing of the payment.

- Transactions are the building blocks of our accounts. Any transactions that occur within our business should be present in our accounting records.

- There are many different types of transactions to keep track of such as sales, purchases, and even more. A regular point of confusion that we come across when we talk to small businesses about their accounts is the difference between cash and credit transactions. So, what is the difference?

- The only difference between cash and credit transactions is the timing of the payment. A cash transaction is a transaction where payment is settled immediately. On the other hand, payment for a credit transaction is settled at a later date.

- Try not to think about cash and credit transactions in terms of how they were paid, but rather, when they were paid. For example, you may buy some groceries at your local shop and pay for them in cash there and then, that’s a cash transaction. However, what if you paid by card rather than cash? That can also be classified as a cash transaction because you paid immediately.

- On the other hand, credit transactions are paid at a later date than when the exchange of goods or services took place and almost all of time an invoice for the transaction is issued. The time period before payment can vary depending on the types of businesses or even the industry in which the transaction is taking place. Once again, when payment is finally settled for the invoice, it may be done with cash or card, or any other payment method but it is still a credit transaction.

- Businesses will have a mixture of cash and credit transactions make up their accounting records. Some businesses may have the majority of their transactions be either one or the other and some will have a more even split. However, you would be hard pressed to find a business that didn’t have at least one cash or credit transaction occur during its lifetime.

- Along with whether a transaction is classified as cash or credit another category is used to classify basic accounting transactions. We also need to know whether or not it is a sale, purchase or payment. This gives us a list of basic transactions:

- 1. Cash sale

- Some of these, like cash and credit sales as well as credit purchases are more common that the others but depending on what type of transaction we have, we can find a home for it in our accounts.

Changing Values of Things Owned and Owed

Sort the changing values of things owned and owed

Accounting standards define an asset as something your company owns that can provide future economic benefits. Cash, inventory, accounts receivable, land, buildings, equipment, these are examples of company's assets. Liabilities are your company's obligations, either money that must be paid or services that must be performed. Example of liabilities include company loan, the money used to pay rent. You should be aware that assets increases company's net worth while liabilities does the opposite.

Assets

Assets refer to resources owned and controlled by the entity as a result of past transactions and events, from which future economic benefits are expected to flow to the entity. In simple terms, assets are properties or rights owned by the business. They may be classified as current or non-current.

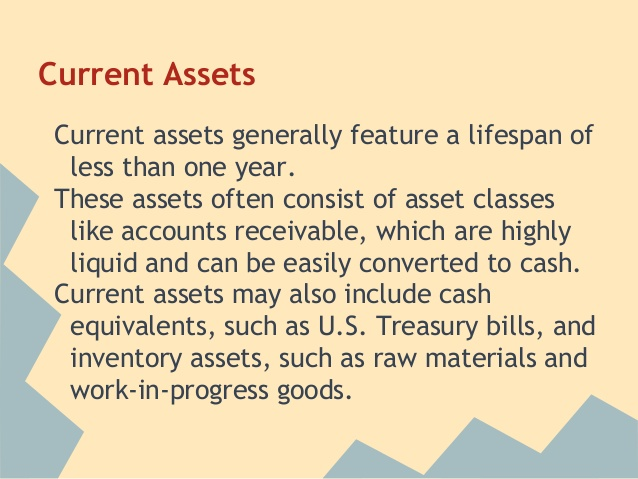

A. Current assets – Assets are considered current if they are held for the purpose of being traded, expected to be realized or consumed within twelve months after the end of the period or its normal operating cycle (whichever is longer), or if it is cash. Examples of current asset accounts are:

- Cash and Cash Equivalents – bills, coins, funds for current purposes, checks, cash in bank, etc.

- Receivables – Accounts Receivable (receivable from customers), Notes Receivable (receivables supported by promissory notes), Rent Receivable, Interest Receivable, Due from Employees (or Advances to Employees), and other claims

- Inventories – assets held for sale in the ordinary course of business

- Prepaid expenses – expenses paid in advance, such as, Prepaid Rent, Prepaid Insurance, Prepaid Advertising, and Office Supplies

• Allowance for Doubtful Accounts – This is a valuation account which shows the estimated uncollectible amount of accounts receivable. It is a contra-asset account and is presented as a deduction to the related asset – accounts receivable.

B. Non-current assets – Assets that do not meet the criteria to be classified as current. Hence, they are long-term in nature – useful for a period longer that 12 months or the company's normal operating cycle. Examples of non-current asset accounts include:

- Long-term investments – investments for long-term purposes such as investment in stocks, bonds, and properties; and funds set up for long-term purposes

- Land – land area owned for business operations (not for sale)

- Building – such as office building, factory, warehouse, or store

- Equipment – Machinery, Furniture and Fixtures (shelves, tables, chairs, etc.), Office Equipment, Computer Equipment, Delivery Equipment, and others

- Intangibles – long-term assets with no physical substance, such as goodwill, patent, copyright, trademark, etc.

- Other long-term assets

• Accumulated Depreciation – This is a valuation account which represents the decrease in value of a fixed asset due to continued use, wear & tear, passage of time, and obsolescence. It is a contra-asset account and is presented as a deduction to the related fixed asset.

Liabilities

Liabilities are economic obligations or payables of the business.

Company assets come from 2 major sources – borrowings from lenders or creditors, and contributions by the owners. The first refers to liabilities; the second to capital.

Liabilities represent claims by other parties aside from the owners against the assets of a company.

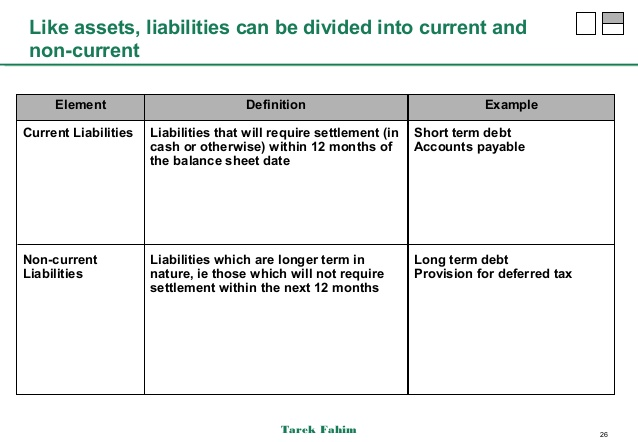

Like assets, liabilities may be classified as either current or non-current.

A. Current liabilities – A liability is considered current if it is due within 12 months after the end of the balance sheet date. In other words, they are expected to be paid in the next year.

If the company's normal operating cycle is longer than 12 months, a liability is considered current if it is due within the operating cycle.

Current liabilities include:

- Trade and other payables – such as Accounts Payable, Notes Payable, Interest Payable, Rent Payable, Accrued Expenses, etc.

- Current provisions – estimated short-term liabilities that are probable and can be measured reliably

- Short-term borrowings – financing arrangements, credit arrangements or loans that are short-term in nature

- Current tax liabilities – taxes for the period and are currently payable

- Current-portion of a long-term liability – the portion of a long-term borrowing that is currently due.

Example: For long-term loans that are to be paid in annual installments, the portion to be paid next year is considered current liability; the rest, non-current.

B. Non-current liabilities – Liabilities are considered non-current if they are not currently payable, i.e. they are not due within the next 12 months after the end of the accounting period or the company's normal operating cycle, whichever is shorter.

In other words, non-current liabilities are those that do not meet the criteria to be considered current. Hah! Make sense? Non-current liabilities include:

- Long-term notes, bonds, and mortgage payables;

- Deferred tax liabilities; and

- Other long-term obligations

Account Balances

Determine account balances

Capital

Also known as net assets or equity, capital refers to what is left to the owners after all liabilities are settled. Simply stated, capital is equal to total assets minus total liabilities. Capital is affected by the following:

- Initial and additional contributions of owner/s (investments),

- Withdrawals made by owner/s (dividends for corporations),

- Income, and

- Expenses.

Owner contributions and income increase capital. Withdrawals and expenses decrease it.

The terms used to refer to a company's capital portion varies according to the form of ownership. In a sole proprietorship business, the capital is called Owner's Equity or Owner's Capital; in partnerships, it is called Partners' Equity or Partners' Capital; and in corporations, Stockholders' Equity.

In addition to the three elements mentioned above, there are two items that are also considered as key elements in accounting. They are income and expense. Nonetheless, these items are ultimately included as part of capital.

Income

Income refers to an increase in economic benefit during the accounting period in form of an increase in asset or a decrease in liability that results in increase in equity, other than contribution from owners.

Income encompasses revenues and gains.

Revenues refer to the amounts earned from the company’s ordinary course of business such as professional fees or service revenue for service companies and sales for merchandising and manufacturing concerns

Gains come from other activities, such as gain on sale of equipment, gain on sale of short-term investments, and other gains.

Income is measured every period and is ultimately included in the capital account. Examples of income accounts are: Service Revenue, Professional Fees, Rent Income, Commission Income, Interest Income, Royalty Income, and Sales.

Expense

Expenses are decreases in economic benefit during the accounting period in the form of a decrease in asset or an increase in liability that result in decrease in equity, other than distribution to owners.

Expenses include ordinary expenses such as Cost of Sales, Advertising Expense, Rent Expense, Salaries Expense, Income Tax, Repairs Expense, etc.; and losses such as Loss from Fire, Typhoon Loss, and Loss fromTheft. Like income, expenses are also measured every period and then closed as part of capital.

Net income refers to all income minus all expenses. See below to see how net income is calculated from gross income. For the employees this is also known as take home.

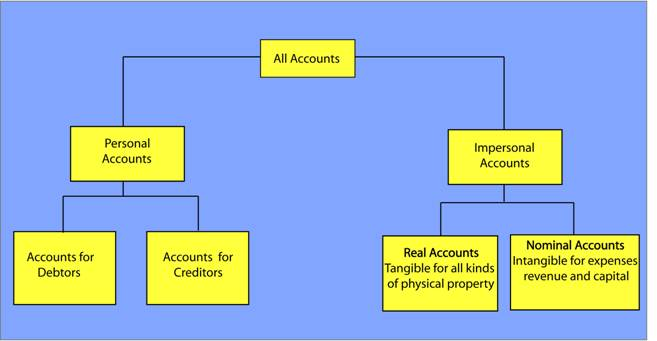

Classification of Accounts

It is necessary to know the classification of accounts and their treatment in double entry system of accounts. Broadly, the accounts are classified into three categories:

- Personal accounts

- Impersonal

- Real accounts

- Tangible accounts

- Intangible accounts

Let us go through them each of them one by one.

Difference between Personal and Impersonal Account

Differentiate between personal and impersonal accounts

The differences between personal and impersonal accounts can be seen from what is debited and what is credited. In this concept you are going to learn those differences and investigate how they differ.

There are two types of accounts. Personal account and impersonal accounts, impersonal accounts is further divided in two groups. They are depicted on the image below.

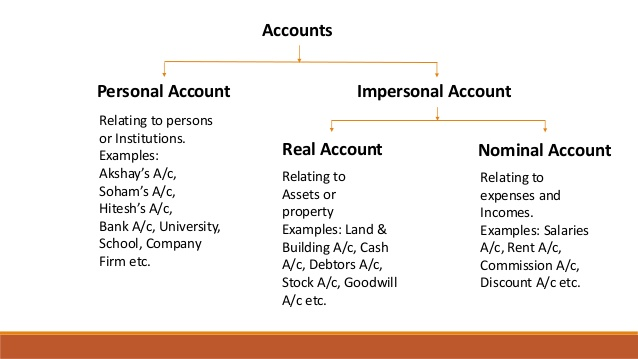

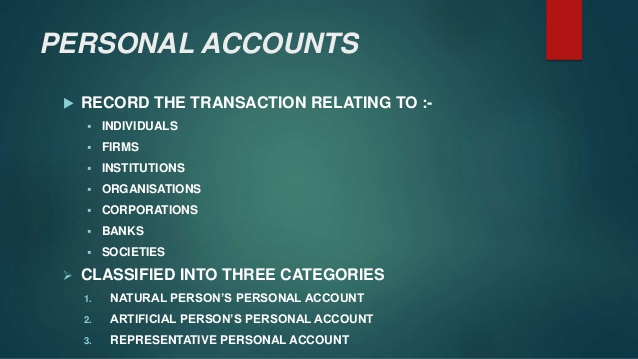

Personal Accounts

Personal accounts deal with accounts relating to individuals, companies, firms and banks. They are further classified into three categories shown below. You will be able to understand them one by one.

Natural Personal Account

An account related to any individual like David, George, Ram, or Shyam is called as a Natural Personal Account.

Artificial Personal Account

An account related to any artificial person like M/s ABC Ltd, M/s General Trading, M/s Reliance Industries, etc., is called as an Artificial Personal Account.

Representative Personal Account

Representative personal account represents a group of account. If there are a number of accounts of similar nature, it is better to group them like salary payable account, rent payable account, insurance prepaid account, interest receivable account, capital account and drawing account, etc.

_1513632177548.png)

Example of personal account

Exercise 1

Explain two types of accounts.What are the difference between real account and nominal account?Think about any account you're owning? Is it personal or impersonal account? Share your answers on the discussion forum.

Trial Balance

Bookkeeping Form 1

You learn about general journals and general ledger on the first topic. In this topic we're going to explore the next process of an accounting cycle which is trial balance. You are going to explore what it is and understand how to prepare it.Lets remind ourselves of an accounting cycle before we start to explore about trial balance.

Meaning of Trial Balance

Define the Trial Balance

Trial Balance is a list of closing balances of ledger accounts on a certain date and is the first step towards the preparation of financial statements. It is usually prepared at the end of an accounting period to assist in the drafting of financial statements. Ledger balances are segregated into debit balances and credit balances. Asset and expense accounts appear on the debit side of the trial balance whereas liabilities, capital and income accounts appear on the credit side. If all accounting entries are recorded correctly and all the ledger balances are accurately extracted, the total of all debit balances appearing in the trial balance must equal to the sum of all credit balances.

Purpose of a Trial Balance

- Trial Balance acts as the first step in the preparation of financial statements. It is a working paper that accountants use as a basis while preparing financial statements.

- Trial balance ensures that for every debit entry recorded, a corresponding credit entry has been recorded in the books in accordance with the double entry concept of accounting. If the totals of the trial balance do not agree, the differences may be investigated and resolved before financial statements are prepared. Rectifying basic accounting errors can be a much lengthy task after the financial statements have been prepared because of the changes that would be required to correct the financial statements.

- Trial balance ensures that the account balances are accurately extracted from accounting ledgers.

- Trail balance assists in the identification and rectification of errors.

Construction of Trial Balance

Construct a Trial Balance

Example

The following is an example of what a simple Trial Balance looks like:

| ABC LTD Trial Balance as at 31 December 2011 | ||

| Account Title | Debit | Credit |

| $ | $ | |

| Share Capital | 15,000 | |

| Furniture & Fixture | 5,000 | |

| Building | 10,000 | |

| Creditor | 5,000 | |

| Debtors | 3,000 | |

| Cash | 2,000 | |

| Sales | 10,000 | |

| Cost of sales | 8,000 | |

| General and Administration Expense | 2,000 | |

| Total | 30,000 | 30,000 |

- Title provided at the top shows the name of the entity and accounting period end for which the trial balance has been prepared.

- Account Title shows the name of the accounting ledgers from which the balances have been extracted.

- Balances relating to assets and expenses are presented in the left column (debit side) whereas those relating to liabilities, income and equity are shown on the right column (credit side).

- The sum of all debit and credit balances is shown at the bottom of their respective columns.

The Advantages and Short Falls of the Trial Balance

Give the advantages and short falls of the Trial Balance

View Teacher Notes

Compute-To calculate an answer by use of machine eg a computer or calculator(=solve).

Rectify-To correct something.

Omission-Act of not including something.

Advantages (Objectives of Trial Balance)

- 1. It ensures that the transactions recorded in the books of accounts have identical debit and credit amount.

- 2. Balance of each ledger account has been computed correctly.

- 3. Balance of each and every ledger account has been transferred accurately and on the correct side of the sheet on which trial balance has been prepared.

- 4. The debit and the credit columns of trial balance have been added up correctly.

- 5. Preparation of final accounts is not possible without preparing trial balance first.

- 6. Agreed trial balance is a prima facie evidence of the arithmetical accuracy of the accounting books maintained.

- 7. Errors which are revealed by preparing trial balance (listed below) are rectified even before the preparation of final accounts.

Errors revealed by (the preparation of) trial balance

- If trial balance does not agree, the disagreement may be due to :

- (1) Omission to post an amount into ledger: If an item is not posted from journal or subsidiary book to ledger, two sides of trial balance shall not agree, e.g., if goods sold on credit to A are recorded properly in sales book but not debited to A's account' in ledger, the debit side of trial balance shall fall short.

- (2) Omission to post an amount in trial balance: It is natural if balance 'of an account is not recorded in trial balance the two sides of trial balance shall not agree which is an indication of error in accounts.

- (3) Wrong totalling or balancing of ledger account: If any account in the ledger is wrongly totalled or balanced, then also the trial balance shall not agree.

- (4) Wrong totalling of subsidiary books: If the total of any subsidiary book is wrongly cast, it would cause a disagreement in the trial balance, e.g., if purchase book totaled Rs. 2,500 instead of 2,050, the debit side of the trial balance shall exceed the credit side by Rs. 450.

- (5) Posting on the wrong side: When an item is by mistake posted on the wrong side of the ledger account it would cause disagreement in the trial balance, e.g., if Rs. 200 have been allowed as discount and while posting into discount account the amount has been credited to discount account. It will result in a difference of Rs. 400 in two sides of trial balance.

- (6) Posting of wrong amount: If wrong amount is posted in one of the two accounts while posting, it would immediately cause disagreement of trial balance e.g. goods worth Rs. 690 have been sold to 'X' but 'X's account has been debited with Rs. 960. It will increase the debit side of trial balance by Rs. 270.

Trial Balance Limitations - Shortcomings of trial balance

- An agreed trial balance does not prove by itself that :

- 1. All transactions have been correctly analyzed and recorded in proper accounts. For example wages paid for installation of fixed asset might have wrongly been debited to wages account.

- 2. All the transactions have been recorded and nothing has been omitted.

- 3. Certain types of errors (listed below) remain undetected even after the preparation of trial balance.

Exercise 1

1. Why is it very important for a company to prepare a trial balance?2. What will happen to a company's financial statement if a trial balance will have a lot of errors?3. What is an accounting cycle?

Trial Balance

Bookkeeping Form 1

Final accounts give a concise idea about the profitability and financial position of a business to its management, owners, and other interested parties. All business transactions are first recorded in a journal. They are then transferred to a ledger and balanced.

These final tallies are prepared for a specific period. The final accounts consist of trading account, profit and loss account, and balance sheet.

Trading, Profit and Loss Account

Describe what a Trading, profit and Loss account is

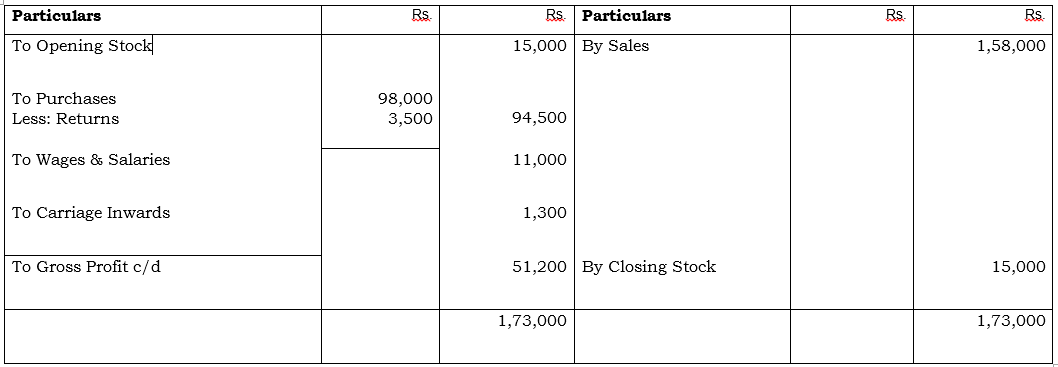

Trading account are those accounts prepared at the end of accounting period for the determination of gross profit or gross loss of the business.

GROSS PROFIT=SALES-COST OF GOODS SOLD

PROFIT AND LOSS ACCOUNT;

A profit and loss statement (P&L) is a financial statement that summarizes the revenues, costs and expenses incurred during a specific period of time, usually a fiscal quarter or year. These records provide information about a company's ability –or lack thereof –to generate profit by increasing revenue, reducing costs, or both. The P&L statement is also referred to as "statement of profit and loss", "income statement," "statement of operations," "statement of financial results," and "income and expense statement."

NET PROFT=NET PROFIT & OTHER INCOME-TOTAL EXPENSES.

EXAMPLE

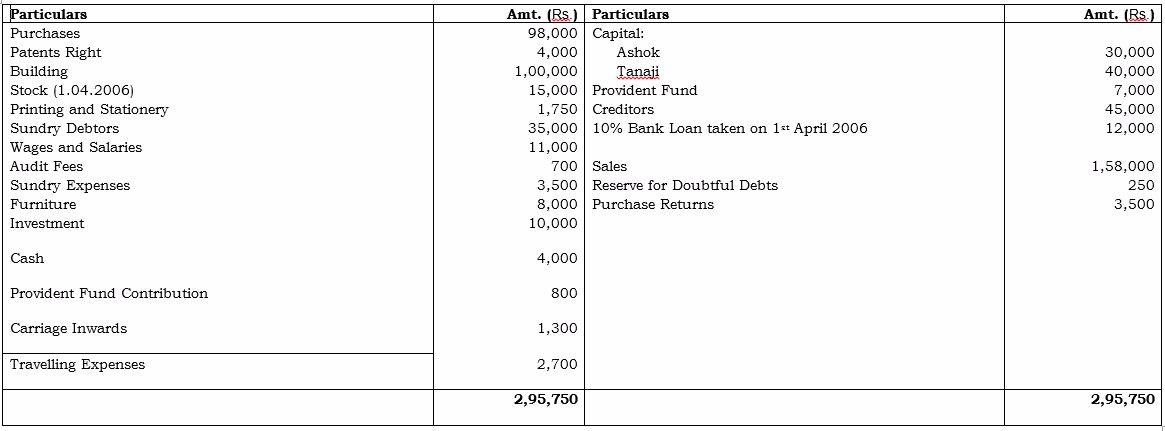

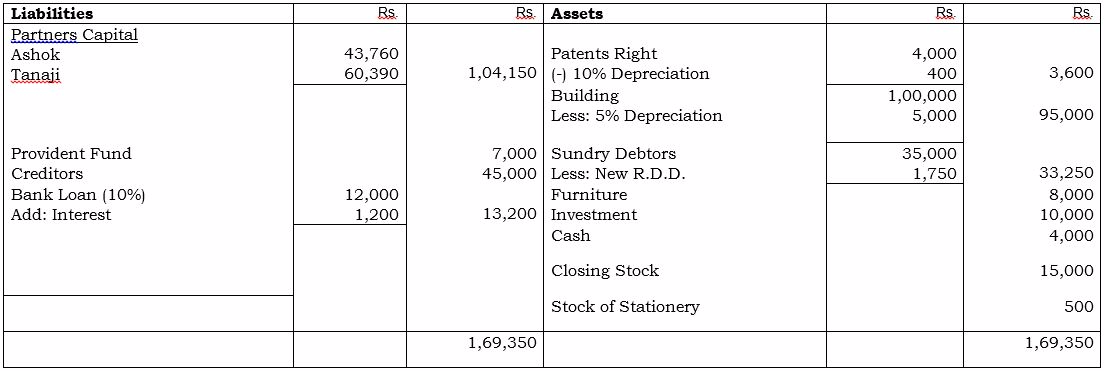

Ashok and Tanaji are Partners sharing Profit and Losses in the ratio 2:3 respectively. Their Trial Balance as on 31st March, 2007 is given below. You are required to prepare Trading and Profit and Loss Account for the year ended 31st March, 2007 and Balance Sheet as on that date after taking into account the given adjustments.

Trial Balance as on 31st March, 2007

Adjustments:

- Closing stock is valued at the cost of Rs. 15,000 while its market price is Rs.18,000.

- On 31st March, 2007 the stock of stationery was Rs. 500.

- Provide reserve for bad and doubtful debts at 5% on debtors.

- Depreciate building at 5% and patent rights at 10%.

- Interest on capitals is to be provided at 5% p.a

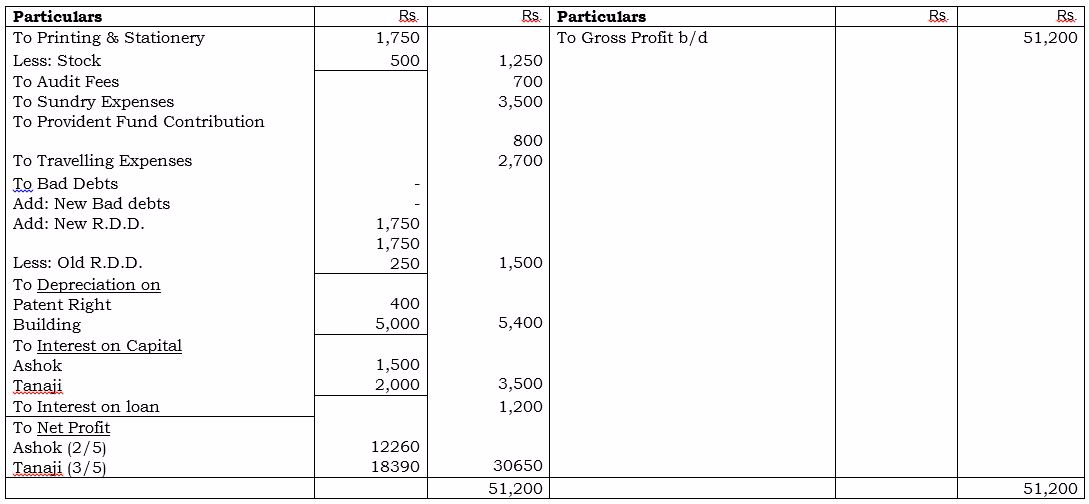

Trading Account for the year ended 31st March 2007

Gross Profit or Gross Loss

Determine the Gross profit or Gross Loss

View Teacher Notes

Fiscal quarter-Consecutive three month period within a fiscal year for which a business reports its result.

Profit & Loss A/c for the year ended 31st March 2007

Partner’s Capital A/c

Balance Sheet as on 31-3-2007

The Cost of Goods Sold

Determine the cost of goods sold

Activity 1

Determine the cost of goods sold

The Net Profit and the Net Loss

Determine the net profit and the net loss

Activity 2

Determine the net profit and the net loss